How Rising Interest Rates Affect Home Buyers in Las Vegas

Buying a home in Las Vegas is an exciting step. From new builds in Summerlin to family-friendly communities in Henderson, the real estate market here offers something for everyone. But one factor shaping the decisions of home buyers right now is rising interest rates. Mortgage rates play a big role in how affordable a home really is, and many buyers wonder what higher rates mean for their budget, loan options, and long-term financial stability.

In this article, we’ll break down how rising interest rates affect home buyers in Las Vegas, what it means for affordability, and what strategies you can use to still achieve your dream of homeownership.

Why Do Interest Rates Matter for Home Buyers?

When you buy a home, chances are you’ll need a mortgage. Your interest rate determines how much you’ll pay the lender over time. Even a small increase can make a noticeable difference in your monthly payment.

For example:

- A $350,000 home with a 5% interest rate might cost around $1,880 a month (principal and interest).

- At 7%, that same loan jumps to about $2,330 a month.

That’s nearly $450 more each month—money that could otherwise go toward savings, upgrades, or day-to-day expenses.

In a city like Las Vegas, where the housing market is competitive, rising interest rates can affect not only what you can afford but also how quickly homes sell.

The Las Vegas Housing Market and Rising Rates

Las Vegas has long been an attractive market for buyers moving from other states, especially California, because of relatively affordable housing and no state income tax. However, with interest rates rising, buyers are noticing:

- Reduced purchasing power– Many buyers now qualify for smaller loan amounts than they did a year or two ago.

- Slower price growth– Home prices may level out as higher rates cool demand.

- Increased competition for affordable homes– Entry-level homes are in even greater demand since higher rates make luxury properties less attainable.

For local buyers, this means adjusting expectations. For out-of-state buyers, it could mean comparing Las Vegas homes not only to prices in their former city but also to their new borrowing costs.

How Higher Rates Affect Loan Programs

Not all mortgages react the same way to rising rates. Depending on your financial situation, you may still find options that keep homeownership within reach.

FHA Loans

For many first-time buyers, FHA loan programs in Las Vegas remain a strong option. FHA loans often come with lower down payment requirements and more flexible credit standards. While interest rates affect FHA loans just like conventional ones, the lower barriers to entry can make them a practical choice even in a higher-rate environment.

Adjustable-Rate Mortgages (ARMs)

Some buyers turn to ARMs, which typically start with a lower rate than fixed-rate mortgages. This can help lower initial payments, though rates may rise later.

Refinancing Options

If you buy at a higher rate today, you’re not locked in forever. Down the road, you can explore options to refinance your mortgage if rates drop again, potentially lowering your monthly payment.

Budgeting and Affordability in a Higher Rate Environment

When interest rates rise, it’s essential to revisit your budget. Homeownership involves more than just the mortgage—it also includes property taxes, insurance, utilities, and HOA fees (common in Las Vegas communities).

Here are a few strategies:

- Get pre-approved early– This helps you understand exactly what you can afford at current rates.

- Consider a slightly smaller home or different neighborhood– Expanding your search beyond the Strip-adjacent areas can uncover more affordable options.

- Look at debt management– If high-interest debts are weighing on your ability to qualify, exploring debt consolidation solutions could improve your financial standing and increase your mortgage options.

What Rising Rates Mean for Sellers—and Buyers

While higher interest rates create challenges, they also open opportunities.

- For buyers: Slower price growth and reduced competition from investors may give you more negotiating power.

- For sellers: Homes may take longer to sell, and pricing competitively becomes more important.

In Las Vegas, where the market has been fast-moving for years, rising rates may create a more balanced environment. Buyers who were once outbid may now have a better shot at securing the home they want.

Long-Term Perspective: Why Buying Still Makes Sense in Las Vegas

Even with rising rates, buying a home in Las Vegas can still be a wise investment. Consider:

- Rent vs. Buy– Rental prices in Las Vegas continue to rise, and monthly rents can rival or exceed mortgage payments.

- Equity Building– Owning a home allows you to build equity, which is not possible when renting.

- Future Refinancing– Today’s rates might seem high compared to a few years ago, but historically they’re still within normal ranges. Buying now means you can refinance later if rates decline.

For buyers planning to stay in their home for several years, the benefits of ownership often outweigh the temporary challenges of higher interest rates.

Tips for Navigating the Current Market

- Work with an experienced local team– Navigating the Las Vegas housing market requires insight into neighborhoods, builders, and financing programs.

- Stay flexible– Have a list of must-haves and nice-to-haves to widen your options.

- Focus on long-term value– Don’t just buy for today’s rate; think about how the home fits your lifestyle and goals over the next 5–10 years.

- Lean on mortgage solutions– Explore FHA, conventional, and refinance options to find the right fit for your budget.

Final Thoughts

Rising interest rates are changing the landscape for home buyers in Las Vegas, but they don’t have to put their homeownership dreams on hold. By understanding how rates affect your budget, exploring flexible loan programs, and planning for the long term, you can still find the right home in this vibrant city.

At Derek Parent Team, we help buyers navigate today’s market with personalized mortgage solutions, whether it’s through FHA loan programs in Las Vegas, refinancing options, or debt consolidation solutions to strengthen your financial foundation.

Las Vegas remains a city of opportunity, and with the right guidance, you can make smart moves—even in a higher interest rate environment.

Gifting a Home

Are you planning on gifting a home to someone this holiday season? For most people, a gift this generous is probably out of the question. But maybe you had a good year financially, and a family member needs the help. Whatever the case is, here are some guidelines when it comes to giving the gift of real estate.

Buying a new home outright

Instead of buying a new home outright, it may be wise to gift the cash for the home, NOT the home itself. Everyone has their own preferences when it comes to what they want in a home, so allowing the recipient of your generous gift to choose their home is probably a much safer idea.

We highly recommend running this by your accountant, as you may also need to file a gift tax return.

Gifting the down payment

Gifting money for a down payment works in pretty much the same way—except when it comes to the mortgage. If there’s even the slightest hint that the money is a loan rather than a gift, it can hinder the recipient’s ability to get a mortgage.

You’ll want to work closely with the recipient’s lender to file the appropriate paperwork, which will include a verified gift letter certifying the funds are a gift, not a loan. The lender will also likely need to examine your finances to determine if you’re able to gift. And remember, most lenders won’t permit gifts from nonfamily members.

Gifting an existing home

Would your children love to own the home they grew up in? Unfortunately this is a poor option, especially if both parents are still living.

One of the tricky struggles with gifting a home you own is the differential between the cost basis (what you first paid for the house) and the current fair market value—which could be hundreds of thousands of dollars, depending on how long you’ve owned it and the appreciation in the area.

This might not matter if your children plan to live in the home forever: The gift will be subject to your gift tax limit, and they’ll only pay capital gains tax if they sell. But if (and, likely, when) they sell, they’ll be stuck paying taxes on the difference.

If you’re determined to gift someone a home this holiday season, remember to keep these guidelines in mind. It IS possible, but of course it’s extremely important to consult your accountant and/or financial advisors to ensure it’s done in the right way.

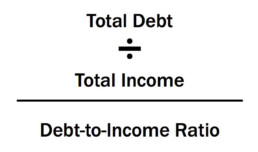

Debt vs. Income: What You Need to Know

Income is a crucial component lenders consider when granting you a mortgage. However, income is not all that a lender will consider when determining how much you qualify for. They will also look at your debt to income ratio, in addition to other financial indicators.

If you make a lot of money but also have a lot of debt, this could be a red flag to lenders and reduce your borrowing capacity.

How debt & income affect your mortgage

Income and debt are yin and yang, opposites of each other. Debt is a liability, whereas the more income you have, the more power you have to make those liabilities go away. Having more income also gives more control of the following.

- It allows you to prepay your mortgage faster.

- It allows you to qualify for more when buying a home.

- It allows you to move into a shorter and more aggressive debt pay-down structure such as a 15-year fixed-rate mortgage.

- It allows you to pay off your credit cards in full every month, rather than paying unnecessary and pricey interest (assuming you’re making smart financial choices).

- It allows you to consume smart debt, such as purchasing a rental property that can generate even more income.

- It allows you to make investments, generating more income.

- It allows you to save and plan for the future.

Having this control over these and other financial choices is precisely why it is CRUCIAL to carry a debt-to-income ratio no bigger than 36% of your gross monthly income. The goal when borrowing mortgage money is to put yourself in a position where you can have a life beyond paying it off, while still saving and contributing to your retirement savings.

What you need to consider before you buy

Always remember it takes $2 of income to offset every $1 of debt for a 2:1 ratio for mortgage qualifying purposes.

If you want that fancy Mercedes at an $800 per month car payment, then you’ll need $19,200 a year in extra income or you’ll need to cut a current debt payment of $800 to balance your debt-to-income ratio.

If you want the dream house at $3,500 month, then aim your debt-to-income ratio at 36%—meaning you would ideally want income at $117,000 a year without carrying other consumer obligations in order to afford this mortgage.

When you are thinking about buying a home, also remember to consider what the future holds for your finances. For example, if your monthly expenses will likely increase in the future due to expenses like childcare costs or college tuition, this is something important to keep in mind. By keeping your debt to income ratio below 36% of your gross monthly income, you’ll put yourself in a position to enjoy your new home but also be able to continue saving for your future.

Unexpected Homebuying Roadblocks

Your offer has been accepted on your dream home and you have a down payment, good credit, and little debt. So the escrow process should be a breeze, right? WRONG! There are some surprising deal breakers that can quickly cause the transaction to go south. Here are a few of the most common ones.

Closing Lines of Credit

Maybe you’ve realized you have a few more credit cards than you’d like your lender to see. Time to shut ’em down before they check your credit, right? Not so fast. Closing down multiple accounts could actually ding your credit. Credit is composed of a few key components, the age of an opened account being one biggie. Shutting down multiple accounts will also lower your credit utilization rates, which can be yet another credit killer. Research the impact of any change to your credit before taking action.

Not Calculating the True Cost of your Mortgage Payment

The cost of homeownership goes far beyond a monthly mortgage check. There are HOA fees, maintenance costs, PMI, etc. Make sure you’ve calculated — and recalculated — whether the cumulative costs will be feasible. You don’t want a nasty surprise when you finally crunch your numbers and realize they don’t fit within your current financial circumstances.

Forgetting Maintenance Costs

Remember that you’ll have to spend much more time and money on the dream house with a pool in the backyard. If you simply don’t have the budget for a home with a pool, communicate this to your agent before you start looking at houses. The last thing you want is to end up falling in love with a home you simply can’t afford to maintain.

Assuming Fixtures are Part of the Deal

Make sure you and the seller agree on exactly what will be included — and what the seller will be taking to their new home sweet home. Things such as light fixtures are often assumed to be a part of the package, but if it’s an heirloom chandelier from the seller’s grandma, chances are they’ll consider it fair game to take when they go. Set out clear expectations of what’s staying and what’s going to avoid any confusion or upset.

Buying a home can be stressful, but with a little preparation (and the right lender and real estate agent) things can go relatively smoothly. No matter what happens, remember to stay flexible. Some things may arise that are out of your control. How you respond can ultimately sway the outcome — and hopefully get you the house of your dreams!

What Happens if You Inherit a Mortgage?

Most homeowners have mortgages, and the sad reality is all homeowners die eventually. And, if a homeowner dies with an outstanding mortgage loan, the mortgage company still expects to be paid. Whether the balance owed will be due all at once or can be paid off over time depends on who inherits the home and the state where thedeceased’s estate is being administered.

Who will owe?

If someone dies owing money on a conventional mortgage, the mortgage company must usually be formally notified of the death as part of the probate process. However, if the deceasedtransferred his or her home to a living trust, such notice may be optional. (Sometimes the loan documents require it.)

If the home is owned by spouses and one of them dies, the mortgage company may allow the surviving spouse to make payments without interference since the loan had been extended to both parties.

If, however, the property is inherited by someone else, such as the deceased’s children, or if the home was just in the name of the deceased, the mortgage company may require the new owner to refinance the mortgage or pay the entire loan balance owed within a fairly short period of time. If the new owner is unable to meet its demand, the lender can foreclose on the home. (If the home was ultimately lost to foreclosure, that should not affect the credit of the “heir” because the heir was never personally obligated to pay the mortgage.) Flexibility on the part of the mortgage company in these circumstances is difficult to predict.

What should I do if I can’t pay?

Sometimes, people do not notify the mortgage company of a mortgage holder’s death and simply continue paying the loan. This scenario might happen, for example, if the heir to the home has bad credit, cannot afford to refinance or, alternately, pay the entire balance due, and yet wants to hold on to the house.

This strategy, however, could blow-up in the heir’s face should the mortgage company discover the ruse because the mortgage documents themselves will allow a foreclosure if the company is not notified of the death within a specific period of time.

All 50 states have laws that regulate mortgages at death. The very best option is to consult with an experienced estate attorney in the state where the home is located. That way, you can learn what specific options you may have.

This article was written by Brad Wiewel and originally published on Credit.com.

What's the Difference Between Getting Pre-approved & Pre-qualified?

Many people mistakenly believe that getting pre-approved for a mortgage is the same thing as getting pre-qualified. They are NOT the same! Here's the difference:

Getting Pre-qualified

Most sellers will require your pre-qualification letter before they’ll even consider your offer. Ask your lender for a prequalification letter. These are relatively simple to get and they just give a rough, unverified estimate of the loan size you may qualify to receive. Most lenders will give you a pre-qualification based on your verbal self-reporting of your income, assets, debts, and down payment size.

Estimated time: 2–3 days

Getting Pre-approved

The pre-approval stage is when lenders verify everything you’ve told them. You’ll need to supply proof of income, proof of assets, proof of employment, records of any debts you hold, and of course identification documents (such as your Social Security card) and a credit report (which the lender will run).

Once you’re pre-approved, you’ll receive a letter stating the exact amount of loan for which you’re approved.

Estimated time: 1 week to several months.

3 Things to Know about FHA Loans

FHA loans are popular with mortgage borrowers because of lower down payment requirements and less stringent lending standards.

Simply stated, an FHA loan is a mortgage insured by the Federal Housing Administration, a government agency within the U.S. Department of Housing and Urban Development. Borrowers with FHA loans pay for mortgage insurance, which protects the lender from a loss if the borrower defaults on the loan.

Less-than-perfect credit is OK

Minimum credit scores for FHA loans depend on the type of loan the borrower needs. People with credit scores under 500 generally are ineligible for FHA loans. The FHA will make allowances under certain circumstances for applicants who have what it calls "nontraditional credit history or insufficient credit" if they meet requirements. Ask your FHA lender or an FHA loan specialist if you qualify.

Lender must be FHA-approved

Because the FHA is not a lender, but rather an insurer, borrowers need to get their loan through an FHA-approved lender (as opposed to directly from the FHA). Not all FHA-approved lenders offer the same interest rate and costs -- even on the same FHA loan.

Costs, services and underwriting standards will vary among lenders or mortgage brokers, so it's important for borrowers to shop around.

Closing costs may be covered

The FHA allows home sellers, builders and lenders to pay some of the borrower's closing costs, such as an appraisal, credit report or title expenses. For example, a builder might offer to pay closing costs as an inducement for the borrower to buy a new home.

Borrowers can compare loan estimates from competing lenders to figure out which option makes the most sense.

Divorce? The 5 Worst Money Mistakes

Written by Guest blogger: Leslie Thompson

During a divorce, a spouse who hasn’t been involved in the family’s finances can often be at a disadvantage during settlement negotiations. That’s why it’s so important for both spouses in the process of dissolving their marriage to understand their post-divorce financial needs and their current financial situation.

The following five items are often overlooked as part of the settlement process, but they’re vital areas to address:

- Cash flow needs

Understanding your need for immediate cash flow is extremely important in determining which assets would be the most beneficial for you to receive in the divorce. If immediate cash flow is a concern, the most valuable assets for you are ones you could sell easily and quickly (so-called liquid accounts), such as stocks, bonds, mutual funds and possibly Roth retirement accounts.

If immediate cash flow is not an issue, a combination of assets with various degrees of liquidity (taxable and retirement plan accounts) will likely be more beneficial long-term.

- Joint liabilities

Just because you agree to split a liability does not mean that the lender will honor your property-settlement agreement. Mortgages will need to be refinanced (if possible), any outstanding tax liabilities on jointly-filed returns will need to be paid and jointly-held credit cards will need to be canceled.

It is important that all liabilities are settled before completing a divorce, either by paying them off or by transferring them to the spouse taking responsibility for the debt.

It is also a good idea to run a credit report to determine if there are any outstanding debts that need to be addressed before settlement.

By securing proof that all liabilities have been settled before the divorce finalization, you’ll avoid an unpleasant surprise when a creditor demands payment from you for a liability that you thought had been settled.

- Taxes on assets

It’s critical to review the tax impact of your investments when evaluating the division of your assets. While two assets or investment accounts may have equal dollar values, their economic value could be vastly different when taxes are factored in.

For example, Roth IRA and Roth 401(k) accounts are funded with after-tax dollars; their future growth and distributions are tax-free. On the other hand, traditional 401(k)s and deductible IRAs are funded with pretax dollars and when you withdraw money from them, taxes will be due on both the amount you contributed and the growth of the investments. As such, Roths have a higher economic value than non-Roth 401(k) or deductible IRAs because they won’t be reduced by future taxes.

If you are younger than 59 and a half, you will pay income tax on withdrawals from non-Roth retirement accounts and possibly a 10% tax penalty. But you can avoid the 10% penalty if the distribution occurs within 12 months following a divorce.

You’ll also want to think about any unrealized capital gains on your taxable investments, since taxes will be due someday. Keep in mind that the first $250,000 of gain from the sale of a principal residence is sheltered from tax.

- Past tax returns

It’s a good idea to review the past three to five years of the tax returns you filed as a married couple. Aside from showing you how much income you two had in a given year, you’ll see whether there are any assets on the settlement agreement or if there are what are known as “tax assets” that need to be considered in the negotiation — such as capital loss carry-forwards, charitable contribution carry-forwards or net-operating losses.

“Tax assets” provide the user a reduction in future taxes and should be considered an asset when splitting the marital estate. But left unresolved, they can cause confusion or errors when filing future tax returns.

- Division of retirement assets

Retirement assets typically represent a large portion of a couple’s net worth and there are special rules to allow for the transfer to be tax-free. You’ll want to make sure the intricacies of these transfers are handled with care.

The divorce decree should specify that any IRA is to be treated as a “transfer incident to divorce” to avoid having the transfer classified as a taxable distribution. Be sure to determine if any basis exists from after-tax contributions made to the IRA — an amount that will be tax-free when distributed. (Consult a tax adviser on this.)

Employer-sponsored retirement plans transfer through a qualified domestic relations order, which requires specific information and approval by the court and plan administrator to allow for a tax-free qualified transfer.

Leslie Thompson is Managing Principal of Spectrum Management Group in Indianapolis. With over 20 years of financial industry experience, she has holds the Chartered Financial Analyst, Certified Divorce Financial Analyst and Certified Public Accountant designations.

*This blog is for information purposes only. Derek Parent and NFM, Inc. accept no liability for its content. Please consult a tax adviser or legal counsel for more information.*