2026 Housing Market Outlook: What Las Vegas Homebuyers Should Know

As we look ahead to 2026, many buyers are asking the same question: What will the Las Vegas housing market really look like? After years of rapid appreciation, rising interest rates, and shifting buyer behavior, the market is entering a new phase—one that rewards preparation, patience, and smart strategy.

Here’s what homebuyers in Las Vegas should know as 2026 approaches.

1. The Market Is Moving Toward Balance, Not a Downturn

Contrary to some headlines, Las Vegas is not heading toward a housing crash. Instead, the market is stabilizing after years of extreme volatility. Price growth has slowed, inventory has improved modestly, and buyer behavior has become more deliberate.

This shift toward balance benefits buyers because:

- Prices are no longer jumping month over month

- Sellers are more open to negotiation

- Appraisals are more predictable

- Financing strategies matter more than speed

In short, 2026 is shaping up to be a market where informed buyers have real leverage.

2. Home Prices Are Expected to Rise Gradually

Most forecasts point to moderate appreciation, not explosive growth. In Las Vegas, that likely means 3–5% annual price increases in most neighborhoods, with stronger performance in high-demand areas such as Summerlin, Henderson, and the Northwest Valley.

What’s supporting prices:

- Continued population growth

- Limited resale inventory

- Strong job creation

- Out-of-state migration

- Few distressed sellers

For buyers, this means waiting for prices to drop significantly may not be realistic. The better strategy is buying when the numbers work—and letting time build equity.

3. Mortgage Rates May Improve, But Timing Matters

Interest rates remain one of the biggest wild cards heading into 2026. While no one expects a return to 3% mortgages, many economists anticipate gradual rate improvement as inflation cools and economic policy stabilizes.

Even a modest rate drop can:

- Increase buying power

- Bring more buyers back into the market

- Reduce seller concessions

- Increase competition

This is why many buyers are choosing to buy before rates improve—then refinance later—rather than waiting and competing with a larger buyer pool.

4. Inventory Will Improve, but Still Favor Sellers

New construction is expanding across Las Vegas, especially in:

- Summerlin West

- Henderson

- Skye Canyon

- North Las Vegas

However, many current homeowners are holding onto low-rate mortgages and choosing not to sell. That limits resale inventory and keeps supply tight.

What this means for buyers in 2026:

- More options than recent years

- Fewer bidding wars than peak markets

- Still strong demand for move-in-ready homes

This isn’t a buyer’s market—but it’s far more navigable than it was just a few years ago.

5. New Construction Will Play a Bigger Role

Builders are expected to remain aggressive heading into 2026, especially with incentives designed to offset affordability challenges.

Buyers may see:

- Closing cost credits

- Temporary rate buydowns

- Discounted upgrades

- Incentives on quick move-in homes

For many buyers, new construction may offer better overall value than resale—especially when incentives are factored into the total monthly payment.

6. High-Rise and Condo Markets Are Strengthening

Las Vegas high-rise and condo markets are quietly improving. As litigation clears in some buildings and financing options expand, buyer confidence is returning.

By 2026, expect:

- More financing availability

- Continued demand from out-of-state buyers

- Stable pricing in premium towers

- Strong interest in low-maintenance living

This is especially relevant for professionals, retirees, and investors seeking convenience and long-term value.

7. Preparation Will Be the Biggest Advantage

The buyers who succeed in 2026 will not be the ones trying to time the market perfectly—they’ll be the ones who are prepared.

That means:

- Getting pre-approved early

- Understanding loan options

- Comparing scenarios (buy now vs. wait)

- Knowing which neighborhoods align with long-term goals

- Working with a local expert who understands Las Vegas market cycles

At The Parent Team, we help buyers analyze these factors clearly—so decisions are based on data, not headlines.

Final Thoughts

The 2026 Las Vegas housing market is shaping up to be one of the most strategic buying environments in years. Prices are stabilizing, inventory is improving slightly, and financing options are evolving. For prepared buyers, that combination creates opportunity.

If you’re thinking about buying in 2026—or want to position yourself early—connect with The Derek Parent Team. We’ll help you understand your buying power, evaluate timing, and build a plan that fits both today’s market and tomorrow’s goals.

Hidden Costs of Buying a Home Most Buyers Don’t Budget For

Most buyers focus on the purchase price and down payment when planning to buy a home. But in reality, the true cost of homeownership goes beyond the sticker price. Failing to budget for the hidden expenses can turn an exciting purchase into a stressful experience.

In a market like Las Vegas — where HOAs, new construction, and high-rise living are common — understanding these costs upfront is critical. Here’s what many buyers overlook and how to prepare for them.

1. Closing Costs Add Up Faster Than Expected

Closing costs are often underestimated or misunderstood. Depending on your loan type and purchase price, closing costs typically range from 2% to 4% of the home price.

These may include:

- Loan origination and underwriting fees

- Appraisal and credit report fees

- Title insurance

- Escrow fees

- Recording fees

- Prepaid taxes and insurance

While seller credits can help offset these costs, buyers should still plan for them early in the process.

2. HOA Fees (A Big One in Las Vegas)

Many Las Vegas communities are governed by homeowners associations, and those monthly dues can vary significantly.

Typical HOA ranges:

- $50–$200/month in suburban communities

- $300–$600/month in condos or townhomes

- $600–$2,500+/month in high-rise buildings

HOA fees are part of your monthly housing cost and can affect loan approval and affordability. They also increase annually in many communities.

3. Property Taxes May Be Higher Than Expected

Property taxes are often estimated, but the actual amount can change after purchase — especially in new construction or recently reassessed homes.

Buyers are sometimes surprised when:

- New construction taxes are reassessed at full value

- Supplemental tax bills arrive after closing

- Escrow payments increase in the second year

Budgeting conservatively for taxes helps avoid payment shock later.

4. Homeowners Insurance Isn’t One-Size-Fits-All

Insurance costs depend on:

- Property type

- Location

- Replacement cost

- HOA coverage (for condos and high-rises)

High-rise and condo buyers may also need HO-6 policies, while single-family homes often require higher coverage for roofs, pools, or detached structures.

Insurance premiums can rise annually, so planning for increases is smart.

5. Utilities and Seasonal Expenses

Las Vegas utility costs — especially electricity — can be significant during summer months.

Buyers often forget to budget for:

- Higher summer power bills

- Gas usage in winter

- Water and sewer fees

- Trash services (sometimes separate from HOA)

A larger home or older property can dramatically increase monthly utility expenses.

6. Maintenance and Repairs

Even brand-new homes come with maintenance costs. Older homes may need repairs sooner than expected.

Common ongoing expenses include:

- HVAC servicing

- Plumbing or electrical repairs

- Roof maintenance

- Appliance replacements

- Landscaping and irrigation upkeep

- Pool maintenance

A good rule of thumb is setting aside 1% of the home’s value annually for maintenance.

7. New Construction Extras

Buyers purchasing new construction often assume everything is included — but many upgrades cost extra.

Common overlooked costs:

- Window coverings

- Backyard landscaping

- Appliances (in some communities)

- Garage finishes

- Smart home upgrades

These expenses often come shortly after closing, so they should be part of your upfront budget.

8. Moving and Setup Costs

The move itself can be expensive.

Don’t forget to budget for:

- Moving services or trucks

- Utility deposits

- Internet and cable setup

- New furniture or appliances

- Minor cosmetic updates

These costs add up quickly, especially if you’re moving from out of state.

How to Avoid Budget Surprises

The best way to avoid surprises is planning early and working with professionals who understand the local market.

At The Parent Team, we help buyers:

- Review full monthly payment breakdowns

- Factor in HOA dues and taxes accurately

- Understand closing costs upfront

- Compare multiple scenarios

- Avoid “payment shock” after closing

A realistic budget leads to a much better homeownership experience.

Final Thoughts

Buying a home is one of the biggest financial decisions you’ll make. While hidden costs can’t always be eliminated, they can be anticipated and planned for.

When buyers understand the full picture — not just the purchase price — they make smarter, more confident decisions and enjoy their home without financial stress.

If you’re preparing to buy and want a clear, honest breakdown of what to expect, connect with The Derek Parent Team. We’ll help you budget accurately and buy with confidence.

What Today’s Interest Rates Really Mean for Las Vegas Buyers

Interest rates dominate real estate headlines, and for buyers in Las Vegas, the noise can feel overwhelming. One-week rates are “coming down,” the next week they’re “higher for longer.” The result? Many buyers are stuck waiting, unsure whether now is the right time to act.

But the reality is more nuanced. Today’s interest rates don’t automatically mean you should stop buying — they simply mean your strategy matters more than it used to.

Let’s break down what today’s rates actually mean for Las Vegas buyers and how to move forward with clarity instead of hesitation.

1. Rates Are Higher — But They’re No Longer Rising Fast

While today’s mortgage rates are higher than the historic lows of 2020–2021, the pace of increases has slowed significantly. That matters.

When rates rise rapidly, buyers freeze. But when rates stabilize — even at higher levels — the market begins to normalize. That’s exactly what we’re seeing now.

For buyers, this creates:

- More predictable monthly payments

- Less emotional decision-making

- Better ability to plan long-term

Stability doesn’t make headlines, but it creates opportunity.

2. Buying Power Has Shifted, Not Disappeared

Yes, higher rates affect affordability. A higher rate means a higher monthly payment on the same purchase price. But that doesn’t mean buying power is gone — it means buyers are adjusting how they buy.

Today’s Las Vegas buyers are:

- Negotiating seller credits

- Using temporary rate buydowns

- Choosing different loan structures

- Being more selective with price and location

In many cases, buyers are paying less upfront than they would have during peak competition years, even if the rate is higher.

3. Prices in Las Vegas Are Holding — Not Collapsing

One of the biggest misconceptions is that higher rates automatically cause prices to drop. In Las Vegas, that hasn’t happened in a meaningful way.

Why?

- Continued out-of-state migration

- Strong job growth

- Limited resale inventory

- Homeowners holding low-rate mortgages

- Ongoing demand in Summerlin, Henderson, and the Northwest

Prices have stabilized, not crashed. That means waiting for a major price correction may not deliver the savings buyers expect.

4. Competition Is Lower — and That’s a Big Advantage

Higher rates have reduced buyer competition, and this is one of the most overlooked benefits of today’s market.

With fewer buyers competing, you’re more likely to:

- Avoid bidding wars

- Negotiate repairs and credits

- Secure seller-paid closing costs

- Take time to make informed decisions

In past years, buyers paid less interest but far more in overbids and waived protections. Today’s buyers often gain leverage instead.

5. Rates Are Temporary — Equity Is Not

Interest rates change. Home prices and equity compound over time.

If you buy today:

- You can refinance later if rates improve

- You lock in today’s price

- You start building equity immediately

- You protect yourself from rising rents

If you wait:

- Prices may rise while rates fall

- Competition may return

- Incentives may disappear

This is why many buyers are choosing to buy the home now and refinance the rate later.

6. New Construction Is Offering Real Value

Las Vegas new construction has become one of the most rate-friendly options for buyers.

Builders are currently offering:

- Rate buydowns

- Closing cost credits

- Discounted upgrades

- Quick move-in incentives

These incentives directly offset today’s interest rates and can dramatically reduce monthly payments in the early years of ownership.

7. The Right Loan Strategy Matters More Than the Rate

In today’s market, success isn’t about chasing the lowest advertised rate — it’s about choosing the right structure.

That may include:

- Temporary buydowns

- Adjustable-rate mortgages (for the right buyer)

- Shorter terms

- Strategic refinancing plans

- Equity-based strategies

This is where working with a local expert makes a measurable difference.

Final Thoughts

Today’s interest rates aren’t a stop sign — they’re a signal to slow down, be strategic, and buy smarter. For Las Vegas buyers, the combination of stabilizing rates, steady prices, reduced competition, and creative financing options creates real opportunity.

If you want to understand how today’s rates affect your buying power, your monthly payment, and your long-term plan, connect with The Derek Parent Team. We’ll help you evaluate real numbers, real scenarios, and real options — so you can move forward with confidence instead of waiting on headlines.

What Credit Score Do You Actually Need to Buy a Home in Nevada?

One of the most common questions buyers ask is also one of the most misunderstood:

“What credit score do I really need to buy a home?”

If you’re buying in Nevada, the answer isn’t a single number. It depends on the loan program, your overall financial profile, and how the lender structures your mortgage.

Let’s break it down clearly—without myths or scare tactics.

The Short Answer: You Don’t Need Perfect Credit

Many buyers assume they need a 740+ credit score to qualify. In reality, many Nevada buyers purchase homes with scores well below that.

What matters most is:

- The loan type

- Your income and debt

- Your down payment

- Your recent credit behavior

Credit score opens doors—but it’s only one piece of the approval puzzle.

Minimum Credit Scores by Loan Type

Here’s how the most common mortgage programs break down.

Conventional Loans

- Minimum score: 620

- Best pricing: 740+

- Down payment options: As low as 3%

Conventional loans reward higher credit scores with better interest rates, but many buyers qualify comfortably in the 620–700 range—especially with solid income and manageable debt.

FHA Loans

- Minimum score: 580 (with 3.5% down)

- Possible with lower scores: 500–579 (with larger down payment, lender-dependent)

FHA loans are popular with first-time buyers because they’re more forgiving of past credit issues. Recent payment history matters more than old mistakes.

VA Loans (for Eligible Veterans)

- No official minimum set by VA

- Most lenders prefer: 620+

- Down payment: 0%

VA loans are one of the most flexible options available. Many veterans qualify even after past credit challenges, as long as current finances are stable.

Jumbo Loans

- Typical minimum: 700–720

- Stronger reserves required

- Higher income verification

Jumbo loans are used for higher-priced homes and require stronger credit profiles—but even here, structure and assets matter.

Why Lenders Look Beyond the Score

A credit score is a snapshot, not the full story. Lenders also evaluate:

- Debt-to-income ratio (DTI)

- Payment history over the last 12–24 months

- Credit utilization

- Derogatory items (collections, late payments)

- Cash reserves after closing

A buyer with a 640 score and low debt may be a better borrower than someone with a 720 score and high monthly obligations.

Common Credit Myths That Hold Buyers Back

Let’s clear up a few misconceptions.

Myth #1: One late payment ruins your chances

Not true. Pattern matters more than one mistake.

Myth #2: You must pay off all collections

Often false. Many collections don’t need to be paid to qualify.

Myth #3: You should close old accounts

Closing accounts can hurt your score by reducing credit history and available credit.

Myth #4: You should wait until your score is “perfect”

Waiting can cost you more in rising prices than you save in rate improvements.

How Much Difference Does Credit Score Make in Your Rate?

Credit score impacts pricing—but not always as dramatically as buyers fear.

For example:

- A buyer at 680 may pay slightly more than a buyer at 740

- But seller credits, buydowns, or refinancing later can offset that difference

This is why many buyers choose to buy now and optimize later, instead of waiting indefinitely.

What If Your Score Isn’t Where You Want It Yet?

If you’re not quite ready today, that’s okay—but guessing isn’t the solution.

A short credit review can:

- Identify what’s helping or hurting your score

- Show which actions actually move the needle

- Prevent unnecessary credit changes

- Create a clear timeline to approval

At https://derekparentteam.com, we help buyers map out specific, realistic steps—not generic advice.

The Most Important Takeaway

The credit score you “need” isn’t a fixed number. It’s about:

- Choosing the right loan

- Structuring the deal correctly

- Understanding what lenders actually care about

Many buyers delay homeownership unnecessarily because of outdated or incorrect credit assumptions.

Final Thoughts

If you’re thinking about buying a home in Nevada, your credit score matters—but it doesn’t need to be perfect. With the right strategy, many buyers qualify sooner than they expect.

If you want an honest review of where you stand—and what’s possible—connect with The Derek Parent Team. We’ll break down your options clearly and help you move forward with confidence.

How Federal Reserve Policy Impacts Mortgage Rates

When mortgage rates rise or fall, most buyers and homeowners hear one phrase repeated over and over: “The Fed did it.”

But the truth is more nuanced.

The Federal Reserve plays a powerful role in shaping the mortgage market — without directly setting mortgage rates. Understanding how Fed policy actually works can help you make smarter decisions about buying, refinancing, or waiting.

Here’s a clear breakdown of how Federal Reserve policy influences mortgage rates and what that means for you as a Las Vegas buyer or homeowner.

1. The Federal Reserve Does Not Set Mortgage Rates

This is the most important point to understand upfront. The Federal Reserve does not directly control mortgage rates.

Instead, it controls:

- The federal funds rate (the overnight rate banks charge each other)

- Monetary policy designed to manage inflation and economic growth

Mortgage rates are primarily influenced by:

- The bond market

- The 10-year Treasury yield

- Inflation expectations

- Investor demand for mortgage-backed securities

However, Fed decisions strongly influence all of these factors — which is why its actions matter so much.

2. Why the Fed Raises and Lowers Rates

The Federal Reserve’s main goals are:

- Control inflation

- Maintain employment stability

- Protect economic growth

When inflation is high, the Fed raises rates to slow spending.

When the economy slows too much, it lowers rates to stimulate growth.

These decisions ripple through financial markets, including housing.

3. How Fed Rate Hikes Push Mortgage Rates Higher

When the Fed raises the federal funds rate:

- Borrowing becomes more expensive for banks

- Investors demand higher returns

- Bond yields rise

- Mortgage-backed securities must offer higher yields to attract buyers

As a result, mortgage rates tend to increase, even though the Fed didn’t touch them directly.

This is exactly what happened during the recent inflation-fighting cycle, when aggressive Fed hikes led to the highest mortgage rates in over a decade.

4. Why Mortgage Rates Sometimes Fall Even When the Fed Holds Rates

This is where many buyers get confused.

Mortgage rates can drop before the Fed cuts rates — or even while the Fed pauses.

Why?

- Investors anticipate future economic slowing

- Inflation expectations ease

- Money flows into bonds as a safe haven

- Demand for mortgage-backed securities increases

Markets move on expectations, not just announcements. That’s why waiting for a Fed rate cut doesn’t always lead to the best mortgage pricing.

5. The Bond Market Matters More Than Headlines

Mortgage rates are closely tied to long-term bonds, especially the 10-year Treasury. When bond yields fall, mortgage rates usually follow.

Key factors that influence bond yields:

- Inflation data

- Employment reports

- Global economic uncertainty

- Federal Reserve guidance and projections

This is why some of the biggest mortgage rate drops happen on days when the Fed doesn’t even meet.

6. What This Means for Buyers

For buyers, Fed policy creates windows of opportunity — but they don’t always line up with news cycles.

Here’s what smart buyers focus on instead:

- Monthly payment affordability

- Purchase price vs. long-term value

- Seller concessions and incentives

- Refinance flexibility later

Trying to time the exact bottom of interest rates is risky. Buying when the numbers make sense — and refinancing later if rates improve — is often the stronger strategy.

7. What This Means for Homeowners

For homeowners, understanding Fed policy helps with:

- Refinance timing

- Cash-out decisions

- Debt consolidation planning

- Equity strategies

Even modest changes in market sentiment — not just Fed action — can create refinance opportunities. That’s why monitoring the bond market and rate trends matters more than waiting for a single Fed announcement.

8. Why Local Expertise Matters

National headlines talk about the Fed. Local experts talk about how Fed policy plays out in your market.

In Las Vegas, factors like:

- Population growth

- New construction incentives

- Investor demand

- High-rise financing conditions

can amplify or soften the impact of Federal Reserve decisions.

At https://derekparentteam.com, we help buyers and homeowners understand how national policy and local market dynamics intersect — so decisions are based on data, not fear.

Final Thoughts

The Federal Reserve sets the tone for the economy, but mortgage rates are driven by a broader mix of market forces. Understanding that relationship helps you stop reacting to headlines and start planning strategically.

Whether you’re buying, refinancing, or simply watching the market, the smartest move is understanding how policy affects real-world numbers, not just announcements.

If you want to see how today’s rate environment — and future Fed policy — impacts your options, connect with The Derek Parent Team. We’ll walk through real scenarios and help you build a plan that works in any market cycle.

What Fannie Mae and Freddie Mac Are Signaling About Mortgage Rates Today

When mortgage rates move, most people look to the Federal Reserve for answers. But inside the mortgage industry, two other institutions quietly provide some of the clearest forward-looking signals about where rates are heading: Fannie Mae and Freddie Mac.

These government-sponsored enterprises don’t set mortgage rates directly, but their forecasts, pricing models, and policy guidance heavily influence lending behavior nationwide. If you’re a buyer, homeowner, or investor trying to decide whether to act now or wait, their signals matter more than most headlines.

Here’s what they’re telling us right now.

Why Fannie Mae and Freddie Mac Matter So Much

Fannie Mae and Freddie Mac back the majority of conventional mortgages in the U.S. Because of that, they closely track economic data tied to housing affordability, inflation, employment, and consumer demand.

When they adjust forecasts or lending assumptions, lenders pay attention — because those changes affect:

- Mortgage pricing

- Loan availability

- Qualification guidelines

- Risk tolerance across the market

In short, they see what’s coming before it shows up in rate sheets.

Signal #1: Rates Are Expected to Ease — Not Collapse

Both agencies are projecting gradual improvement in mortgage rates, not a sudden drop. This is an important distinction.

Their recent outlooks suggest:

- Inflation is cooling, but not gone

- The economy is slowing, not breaking

- Rate volatility is decreasing

- Long-term rates are stabilizing

What this means for buyers is simple: the era of sharp rate spikes appears to be behind us, but the return to ultra-low rates is unlikely.

Translation: Rates may improve, but waiting for perfection could be costly.

Signal #2: Housing Demand Remains Strong

Despite higher rates, both Fannie Mae and Freddie Mac continue to report persistent housing demand, especially in growth markets like Las Vegas.

Key reasons:

- Ongoing population growth

- Limited resale inventory

- Homeowners holding low-rate mortgages

- Rising rents pushing renters toward ownership

This sustained demand is one reason neither agency expects meaningful home price declines in most markets. Instead, they’re forecasting moderate, steady appreciation.

Signal #3: Affordability Is Improving in Subtle Ways

While rates remain elevated compared to prior years, affordability is improving through other channels:

- Slower price appreciation

- More seller concessions

- Builder incentives

- Temporary rate buydowns

- Expanded loan strategies

Fannie Mae has noted that buyers are adapting rather than exiting the market. That adaptability is stabilizing housing activity — and reinforcing the idea that the market is normalizing, not weakening.

Signal #4: Refinance Activity Will Return — Slowly

Both agencies expect refinance volume to increase incrementally, not explosively. Homeowners with rates in the high-6% to 7% range may benefit from refinancing even with modest rate improvements.

What’s especially notable is the growing focus on:

- Cash-out refinances

- Debt consolidation

- Term restructuring (30-year to 20- or 15-year)

- Removing mortgage insurance

This tells us that homeowners are becoming more strategic — using refinancing as a financial tool, not just a rate play.

Signal #5: Lending Standards Are Holding Steady

One of the most important signals from Fannie Mae and Freddie Mac is what isn’t happening: lending standards are not tightening aggressively.

That suggests:

- No systemic housing risk

- No pullback from qualified borrowers

- Continued confidence in the housing market

For buyers, this is a strong indicator that the market is on solid footing — not headed toward instability.

What This Means for Las Vegas Buyers and Homeowners

In growth markets like Las Vegas, these signals matter even more. Continued in-migration, limited inventory, and strong employment trends are aligning with the broader national outlook.

For buyers:

- Waiting for dramatic rate drops may backfire if competition increases

- Buying now with flexibility to refinance later can be a smart strategy

For homeowners:

- Reviewing refinance and equity options sooner rather than later may unlock meaningful savings

- Strategic planning matters more than timing the absolute bottom

The Bigger Picture

Fannie Mae and Freddie Mac aren’t signaling fear. They’re signaling stability, moderation, and opportunity for prepared buyers.

Mortgage rates may not fall overnight, but the environment is becoming more predictable — and predictability creates opportunity for those who plan ahead instead of reacting late.

Final Thoughts

If you’re waiting for a clear sign from the market, this is it: the foundation is stabilizing, demand remains strong, and the smartest moves are happening quietly — before the next wave of buyers re-enters the market.

If you want to understand how today’s signals apply to your situation, connect with The Derek Parent Team at https://derekparentteam.com. We’ll walk you through real numbers, real options, and real strategies — not just headlines.

High-Rise vs. Single-Family Financing: What Buyers Need to Know

When buyers compare high-rise or condo financing to single-family home financing, many assume the loan terms are drastically different. In reality, the financing structure is very similar—but the process is not.

Understanding these differences upfront can save time, reduce stress, and prevent surprises once you’re under contract.

Down Payment Requirements: Very Similar

From a lending standpoint, high-rise and single-family properties generally follow the same down payment guidelines:

-

Primary Residence: 5% down

-

Second Home: 10% down

-

Investment Property: 20% down

These thresholds apply whether you are purchasing a single-family home or a condo in a high-rise building such as Veer Towers or ONE Las Vegas.

The Real Difference: Documentation and Project Approval

Where high-rise and condo purchases differ significantly is in documentation and upfront due diligence.

Condos and high-rise buildings require:

-

HOA certification

-

Condo project approval

-

Budget and reserve analysis

-

Owner-occupancy and rental ratio review

-

Insurance and litigation review (if applicable)

This process ensures the building meets lending guidelines before a loan can be finalized. Single-family homes do not require this level of project review, which is why they often move through underwriting faster.

Why This Matters Before You Write an Offer

High-rise financing is not more difficult—but it does require experience. Missing documentation or an unapproved condo project can delay closing or, in some cases, stop financing altogether.

When handled properly and early in the process, buyers still benefit from:

-

Competitive rates

-

Low down payment options

-

Standard loan programs

-

Smooth closings

The key is working with a lender who understands the condo approval process and can address these requirements before they become an issue.

Bottom Line

High-rise and single-family financing offer similar loan options, but high-rise purchases demand more upfront preparation. The earlier this work is done, the smoother the transaction will be.

If you’re considering a condo or weighing it against a single-family home, having the right guidance early can make all the difference. Let’s have that conversation before you write your offer.

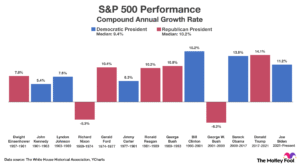

2026 Economic Outlook: What History and Policy Suggest May Be Ahead

As we look ahead to 2026, a research partner recently published a report that does an excellent job framing what we may experience next—especially when viewed through the lens of historical presidential cycles.

While every economic cycle has unique variables, history provides useful context for planning. When paired with current fiscal and monetary policy, it helps explain both recent market performance and what may lie ahead.

The Policy Backdrop Heading Into 2026

When Congress passed the One Big Beautiful Bill, income taxes were not reduced to offset the economic impact of tariffs. As a result, a meaningful amount of stimulus is expected to

flow into the economy in early 2026, including:

- Approximately $150 billion in tax refunds

- Roughly $200 billion in business tax cuts

- Federal Reserve interest rate reductions

- Federal Reserve balance sheet expansion

In addition, the Federal Reserve is proposing to loosen certain bank capital regulations. If implemented, this could unlock an estimated $150–$200 billion of bank capital, much of which could flow into mortgages and the bond market, placing downward pressure on interest rates.

Taken together, these factors point to a highly stimulative economic environment as we move further into 2026.

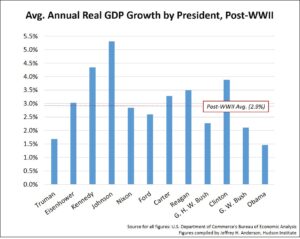

Real GDP Growth and the Presidential Cycle

Historically, real GDP growth has tended to peak during the second year of a presidential cycle. This reflects the delayed effect of fiscal and monetary policy as stimulus works its way into the real economy.

Economic activity often strengthens after policy measures are put in place, even if financial markets have already reacted well in advance.

Financial markets typically anticipate economic activity several calendar quarters ahead. This is why strong market performance often occurs before the real economy shows its full response.

As the chart above illustrates, the S&P 500 has historically produced

strong returns early in a presidential cycle, followed by more muted or slower performance in Year 2, particularly as investors begin to focus on upcoming midterm elections.

This helps explain why recent market performance is no surprise, and why expectations remain for momentum to continue into early 2026. However, once stimulus is firmly embedded and the real economy is clearly responding, markets often pause or consolidate rather than continue moving straight up.

What This Means for Planning

Importantly, this pattern does not signal economic weakness. In many cases, it reflects the opposite:

- A strengthening real economy

- Improving liquidity conditions

- Financial markets that have already priced in much of the good news

For homeowners, buyers, and investors, these environments often create strategic opportunities, particularly around interest rates, refinancing windows, and long-term real estate planning.

Final Thoughts

While no forecast is perfect, understanding how policy, markets, and economic cycles interact can help with smarter decision-making. As we head into 2026, the combination of stimulus, regulatory changes, and historical precedent suggests an environment that rewards planning, patience, and proactive strategy.

If you’d like to discuss how this outlook may impact your personal situation, real estate decisions, or client planning for 2026, I’m always happy to connect.

Wishing you continued success and good health in the year ahead.

Is Now the Right Time to Refinance? A Data-Driven Look at Today’s Market

With interest rates shifting, home values rising, and consumer debt at all-time highs, many homeowners are asking the same question:

“Is now the right time to refinance?”

While the answer depends on your personal financial situation, the current market offers several compelling reasons to take a closer look. Here’s a data-backed breakdown of when refinancing makes sense—and when it might not.

1. Mortgage Rates Are Off Their Highs

After hitting multi-year highs, mortgage rates have begun to stabilize. While they haven’t returned to historic lows, they’ve dropped enough to create meaningful savings for many homeowners.

What the data shows:

- Rates have eased from their peak levels in recent years

- Experts project continued gradual improvement through 2025

- Even a 0.50% to 1.00% improvement can create thousands in long-term savings

If your current mortgage rate is above the market by even half a point, a refinance may help reduce your payment.

2. Home Values in Las Vegas Continue to Rise

Las Vegas remains one of the most stable and desirable real estate markets in the country. Rising home values mean more tappable equity—equity you can use to:

- Consolidate high-interest credit card debt

- Pay for home improvements

- Invest in another property

- Lower your overall financial stress

Many homeowners don’t realize how much equity they’ve gained since 2020. A quick valuation review can reveal whether a refinance or cash-out refinance is a smart move.

3. Debt Levels Are Higher Than Ever

The average credit card interest rate now exceeds 20–30%, and personal loan rates continue to climb. Millions of homeowners are carrying high-interest balances while paying much lower interest on their mortgage.

A cash-out refinance allows you to roll high-interest revolving debt into one low-rate payment—improving cash flow and helping pay off debt faster.

Data point to consider:

Replacing $20,000 in credit card debt at 25% interest with a refinance at 6–7% interest can save thousands per year.

4. Refinancing to Shorter Terms Can Save Big

Many homeowners don’t consider a refinance unless the payment goes down—but refinancing into a shorter term can dramatically reduce interest paid over the life of the loan.

For example:

- A 30-year loan refinanced into a 20- or 15-year loan

- A slightly higher payment but tens of thousands saved in interest

This is a powerful strategy for homeowners planning early retirement or building wealth aggressively.

5. When Refinancing Might NOT Make Sense

A refinance isn’t right for everyone. You may want to hold off if:

- You plan to sell your home within the next 1–2 years

- Your current interest rate is already competitive

- You lack enough equity to qualify for the loan you want

- Closing costs outweigh long-term savings

Your lender should analyze your breakeven point—how long it takes for your monthly savings to outweigh upfront costs.

6. How Long You Plan to Stay Matters

If you plan to keep your home long-term, even modest rate improvement can create significant savings. But if you’re moving soon, short-term benefits may not justify the closing costs.

A quick consultation can determine whether refinancing offers meaningful value based on your goals.

7. Refinancing Is Easier Than Most People Think

Many homeowners worry refinancing will be stressful or time-consuming, but today’s digital process makes it more streamlined than ever.

Most refinances require:

- Income verification

- Home valuation

- Bank statements

- Standard loan disclosures

With a good lending team, the process is often completed in 20–30 days or less.

Final Thoughts

There is no one-size-fits-all answer to refinancing—but today’s market offers strong opportunities for many homeowners. With rates easing, equity rising, and consumer debt increasing, now may be the perfect time to evaluate your numbers.

A data-driven refinance strategy can help you:

- Lower your payment

- Eliminate high-interest debt

- Strengthen your financial profile

- Build long-term wealth

If you want to explore whether refinancing makes sense based on your current rate, equity, and goals, connect with The Derek Parent Team. We’ll run a custom analysis and show you exactly what you could save in today’s market.

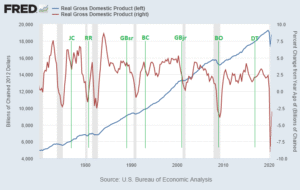

Real GDP Growth Trends: What Economic Cycles Tell Us About the Outlook

Understanding real GDP growth trends is one of the most reliable ways to evaluate the underlying strength of the economy. While short-term data often fluctuates, GDP provides a broader, more stable view of how economic activity evolves over time.

For homeowners, buyers, and investors, GDP trends matter because they directly influence employment, income growth, housing demand, and long-term real estate performance.

How Real GDP Growth Typically Evolves

Historically, real GDP growth tends to strengthen and peak during the middle phase of an economic cycle. This occurs as expansion gains traction through:

- Increased consumer spending

- Higher business investment

- Expanding employment and wage growth

GDP is considered a lagging but confirming indicator. Strong GDP readings often appear after economic momentum is already underway, which is why housing activity and buyer confidence often improve before GDP peaks.

Why GDP Growth Matters for Housing and Real Estate

Strong GDP growth is closely tied to real estate fundamentals. As economic activity expands:

- Job creation supports household formation

- Income growth improves affordability

- Demand for both owner-occupied and investment properties increases

Historically, periods of sustained GDP growth align with healthy housing demand, even if price growth moderates.

This is especially important for buyers evaluating timing, and for homeowners considering long-term equity planning.

How GDP Growth and Financial Markets Differ

Financial markets are forward-looking, often pricing in expectations well before GDP data reflects them. As a result, market performance and GDP growth do not always peak at the same time.

This distinction matters in real estate because housing activity tends to follow real economic conditions, not short-term market sentiment. GDP growth provides confirmation that demand is supported by income and employment—not speculation alone.

GDP Growth and Mortgage Planning

GDP trends also influence mortgage strategy indirectly. Strong economic growth environments often coincide with:

- Increased loan demand

- Greater borrower confidence

- Strategic opportunities for refinancing or purchase planning

Understanding where the economy sits in the growth cycle can help borrowers make more informed mortgage decisions, particularly for long-term financing strategies.

Planning Takeaways for Buyers and Homeowners

For buyers, homeowners, and long-term investors, GDP growth trends help frame expectations around:

- Housing demand sustainability

- Income and employment stability

- Long-term property value support

Strong GDP growth environments tend to reward disciplined planning and thoughtful timing, rather than reactive decision-making.

Final Thoughts on GDP and Economic Cycles

While no single indicator tells the full story, real GDP growth remains one of the most dependable measures of economic health. Historical trends show that GDP often strengthens as economic cycles mature, even when markets appear uneven.

For those making housing or mortgage decisions, understanding GDP trends provides valuable context—helping align real estate strategy with the broader economic environment.

If you’d like to discuss how current GDP trends may relate to housing, real estate, or mortgage planning, I’m always happy to connect.